In the first place, setting up an open-source centre for shared services appears to be a clear success in operation.

The accounts payable (AP) process is centralized

The standard operating procedure is described

The volume of transactions is managed on a large scale

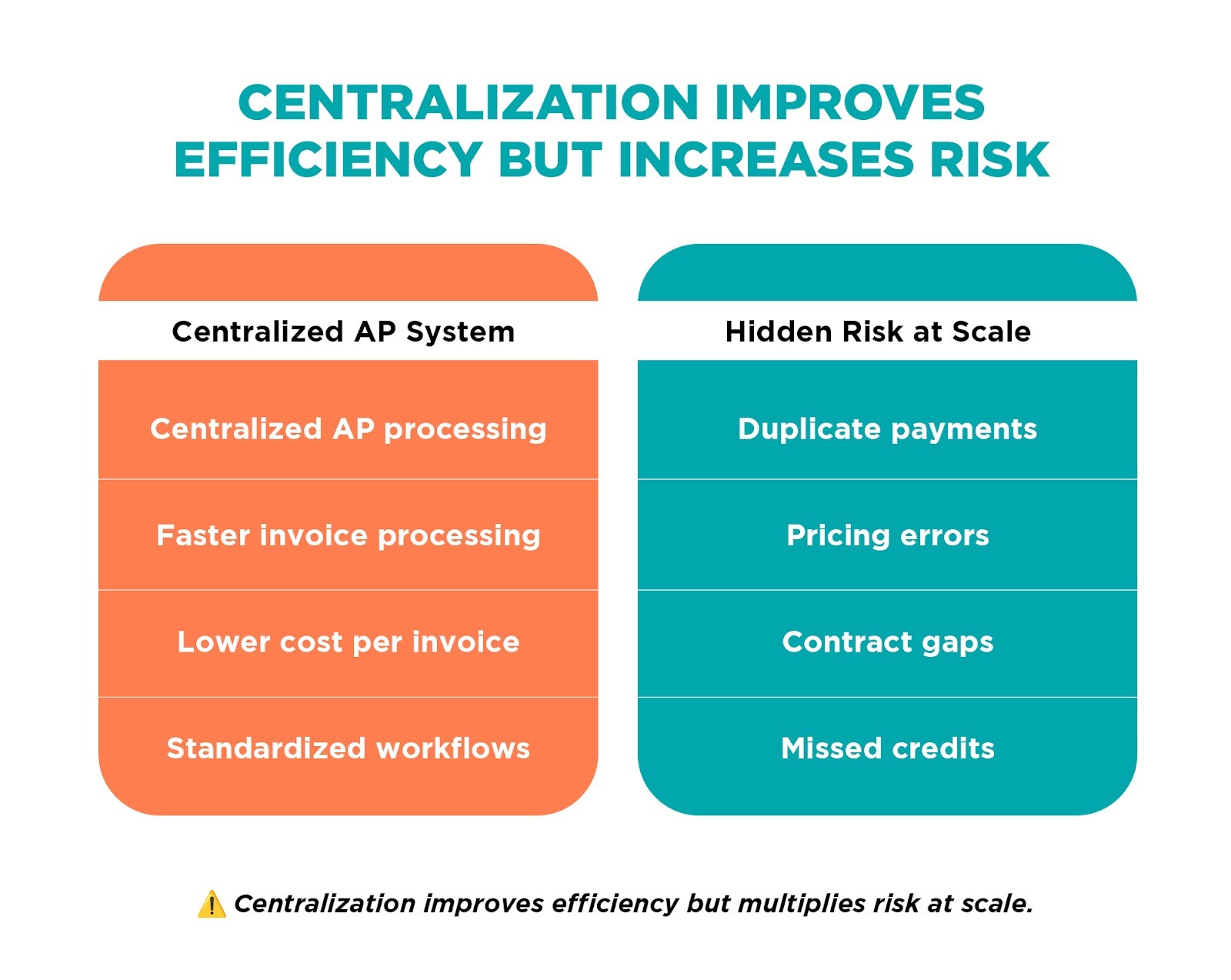

Finance leaders are seeing lower operating costs and better efficiency metrics, such as cycle time and cost per invoice, as well as improved processing efficiency. However, efficiency metrics don't always provide the complete picture.

When companies centralize accounts payable across different entities, business divisions, and geographic locations, they also increase the risk of financial loss. A single process flaw could result in a silent, recurring error across many transactions. When these transactions multiply to millions of invoices each year, minor errors could cause substantial financial leakage.

Centralization Improves Efficiency but Concentrates Risk

Global Business Services (GBS) and shared services centers are designed to maximize execution. Their success is measured using operational KPIs like:

- Invoice processing speed

- Transaction throughput

- Vendor response time

- Cost efficiency

The functions they perform are essential to ensuring operational discipline throughout the procure-to-pay cycle. Yet, the shared service teams aren't structured to spot financial leaks from systems.

Their primary responsibility is operational performance. Examining historical vendor payment anomalies and duplications, pricing discrepancies, and unresolved credit issues is typically beyond their daily responsibilities.

This means that certain issues may persist in high-volume payment systems for many years.

For instance:

- Duplicate payments

- Duplicate vendor invoices

- Pricing errors

- Unclaimed credit notes

- Contractual rebate gaps

Why Shared Services Teams Cannot Self-Detect Financial Leakage

It's a popular myth that ERP, automation, and standardized workflows are the only way to eliminate any payment mistakes.

In the real world, even ERP systems may still suffer from:

- Duplicate invoice postings

- Vendor master data inconsistencies

- Contract pricing mismatches

- Tax or freight misallocations

If organizations use different ERP platforms or vendor databases, the risk is increased.

However, even the best-trained shared service teams work in large-scale processing settings. Their primary concern is ensuring the continuity of processing, not conducting forensic analyses of past transactions.

This is why corporate finance managers establish independently-run financial recovery audits or post-payment audit frameworks to provide an additional layer of financial control.

This method does not replace the use of shared services. Instead, it improves the enterprise's financial management.

The Role of Continuous Recovery Audits in Enterprise Finance

In the past, companies conducted audits of accounts payable every couple of years to ensure compliance.

Today, many leading finance companies are moving towards continuous recovery audits.

Instead of waiting for a review every few months, the programs look at the data of accounts payable regularly to find:

- Duplicate payments

- Vendor overcharges

- Coupons and discounts that are not used

- Pricing discrepancies

- Duplicate tax or freight costs

Since the review occurs after payment, it operates independently of day-to-day AP Processing. A properly-structured AP recovery auditing program makes sure that financial leaks are detected regularly, rather than being discovered years afterward during external or internal audit dists.

Why Corporate Finance Owns Recovery Strategy

Recovery audits are not just operational instruments. They are safeguards for the enterprise's financial security.

This is the reason that the responsibility of implementing accounts payable recovery audits generally falls on:

- Corporate Finance

- CFO offices

- Internal Audit leadership

These stakeholders manage financial risk across the company, including the security of the procure-to-pay system.

Shared services centers continue with a focus on efficiency and execution.

Finance for corporates, in turn, ensures that financial system leaks are independently monitored and, if necessary, retrieved.

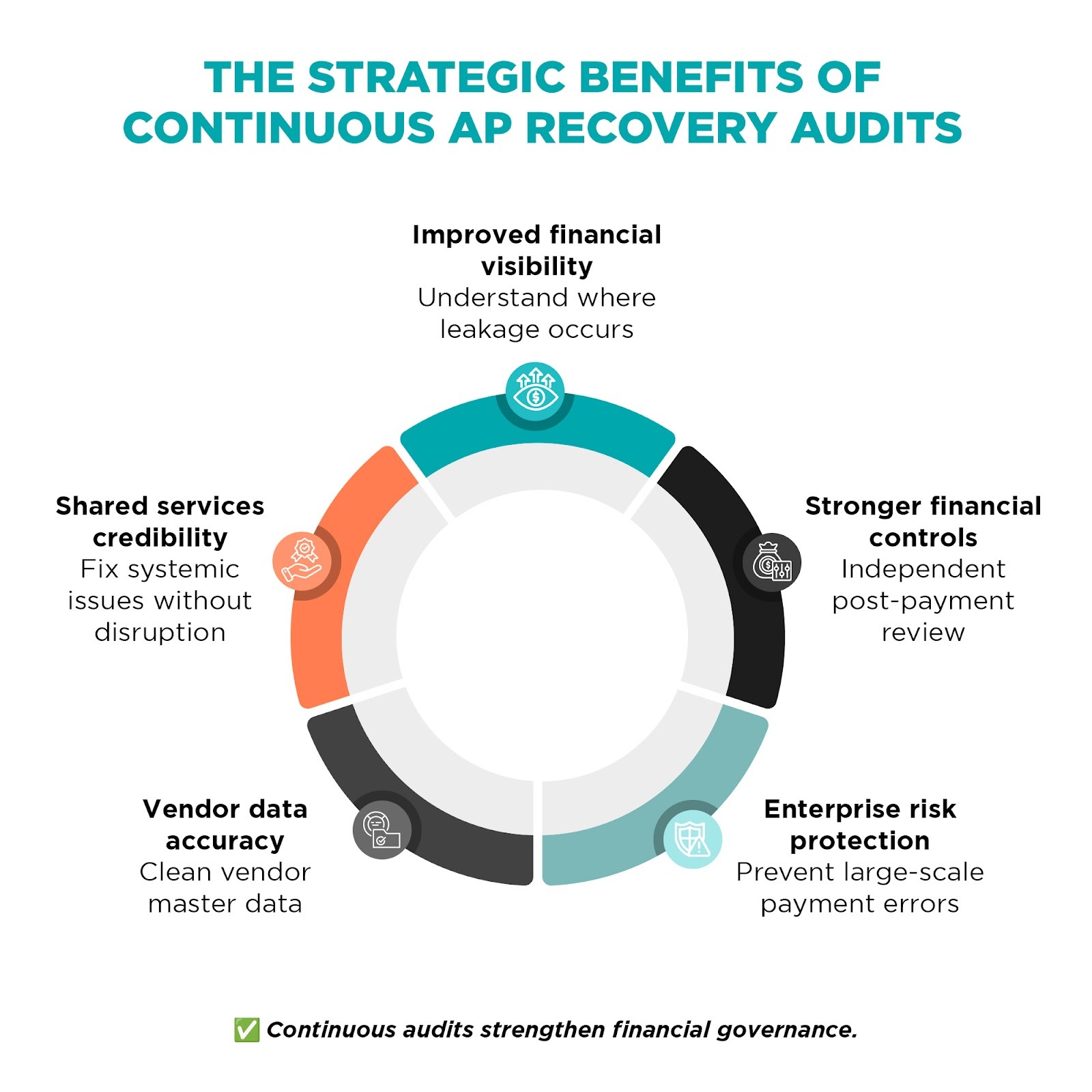

The Strategic Benefits of Continuous AP Recovery Audits

When companies adopt structured financial recovery audit programs, they usually realize benefits that extend beyond recovering payments.

Improved Financial Visibility

Continuous AP analysis of data highlights the frequent errors in contracts, vendor billing, and internal workflows. Finance executives gain a better understanding of the sources of leakage.

Stronger Financial Controls

Recovery audits function as a post-payment monitoring method, in addition to existing procure-to-pay procedures.

Enterprise Risk Protection

Large companies processing millions of invoices each year, even a small amount of billing mistakes can result in an enormous financial burden.

Vendor Data Accuracy

Recovery audits often identify inconsistencies in vendor master data, helping organizations improve their vendor governance.

Reinforced Shared Services Credibility

Instead of criticizing shared services, independent audits of accounts payable recovery actually help them detect and rectify systemic problems without affecting operational KPIs.

Final Words

Centralized accounts payable environments provide effectiveness along with operational discipline. However, the fact that millions of bills pass through a single structure of processing each year, even tiny gap in the system can lead to massive financial leakage.

This is where Discover Dollar plays a crucial role. We are an independently-owned recovery auditing partner, working with global companies in addition to Fortune 500 organizations. With advanced analysis and AI-driven audit technologies, Discover Dollar reviews transactions across ERP systems and entities as well as vendor networks in order to identify the financial leaks that traditional auditing methods typically fail to detect.

For companies that operate large GBS or shared services structures, this separate recovery layer improves financial governance, without affecting operational efficiency. Shared service teams remain focused on achieving the highest level of processing, while corporate finance is able to establish a solid method to safeguard enterprise cash flow.