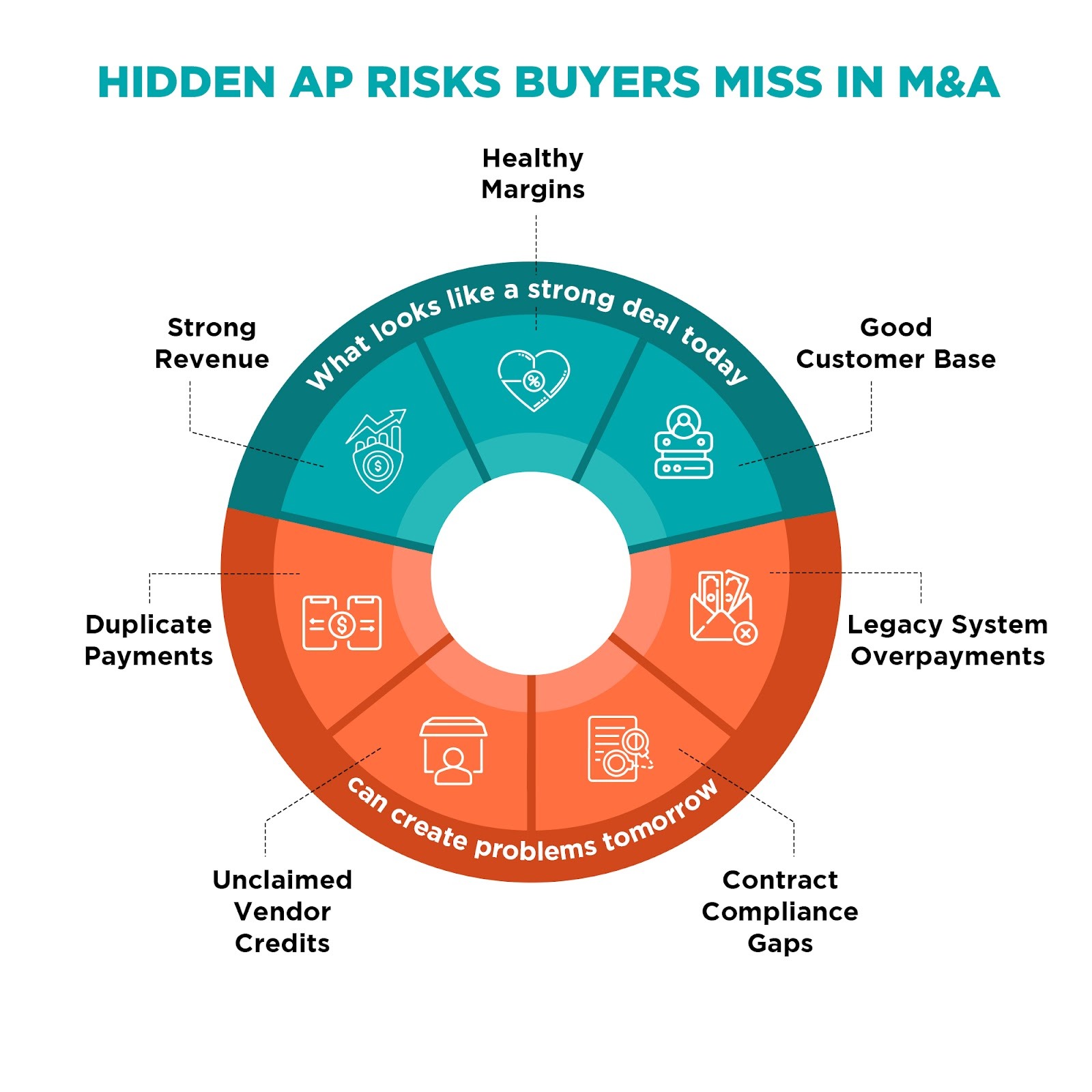

Your potential acquisition is the perfect deal: strong revenue and profit margins, and an attractive customer base.

Your bankers are buzzing with excitement, your lawyers have examined the deal structure, and your advisors have signed off on the valuation.

Then, six months after closing the deal, you learn that the acquired company has overpaid its vendors for three years and unsubscribed from duplicate payment contracts.

Vendor contracts have not been enforced, and there are unclaimed supplier credits. These liabilities are now your company's problem.

The Due Diligence Blind Spot

The M&A due diligence process is designed to be thorough after an acquirer has received its final bid. Financial statements are dissected, customer contracts are examined, and legal, HR, and IT liabilities are scrutinized as an army of advisors is hired to cover all potential blind spots.

However, the same cannot be said for the accounts payable section of the due diligence. Most advisors are fortunate if the purchase agreement includes an accounts payable section in the completion accounts that is designed to understate the purchase price.

Most acquirers treat outstanding accounts payable as a balance sheet liability. As a consequence of that oversight, their due diligence often ignores years of overdue invoice payments, reclaimable credits, contractual compliance gaps, and process breakdowns that represent both liability and untapped recovery potential.

A structured account payable recovery audit supported by specialized accounts payable audit services can reveal these hidden exposures before the deal closes.

What Buyers Overlook

By forgoing an accounts payable recovery audit, buyers are often faced with the following issues after the acquisition:

Payment duplicates

Duplicates are easily created in high-transactional environments. The acquired business may have been processing payments for the same invoices across multiple ERPs, resulting in duplicate payments. It's important to note that duplicates do not appear on the balance sheet; however, funds are missing and should be recovered.

Vendor credits unreconciled

When goods are returned, the vendor issues a billing error, a promotional allowance, or a credit. In many organizations, these credits sit in the accounts payable system unreclaimed, sometimes for years. After an acquisition, recovering these credits becomes even more complicated due to the transfer of vendor relationships and the consolidation of historical records resulting from system migrations.

Failures in contract compliance

The purchased company has entered into agreements with vendors that structure pricing, discounts, and rebates. There has been no systematic verification of compliance. Now you have ownership of these contracts and the history of non-compliance. Vendors have been billing you incorrectly for years, and the mistakes are buried within the data you just acquired.

Overpayments due to legacy systems

Many acquisition targets have undergone numerous ERP system migrations. Such migrations are infamous for duplicate payments and forgotten credits. If the company changed systems two years ago and did not conduct an AP recovery audit, you are left with unresolved problems.

The Impact No One Counts in the Valuation

Most buyers focus only on the identified liabilities during due diligence, and that is where it becomes really interesting from a deal standpoint. But AP leakage impacts the valuation in two very different ways.

On one side, you have hidden liabilities: overpayments to vendors that went uncaught, process breakdowns that will continue to leak money after close, and compliance issues that will provide ongoing financial exposure.

Take, for example, vendor recovery opportunities (money that can actually be retrieved from vendors), unclaimed credits, rebates, etc., which can be included in your recovery prospects.

Both sides affect the true value of your purchase, and both are typically uncovered through targeted accounts payable audit services or a structured account payable recovery audit during diligence.

Why Post-Close Is the Worst Time to Discover This

Vendor disputes are inevitable. Before closing a deal, the vendors of the target company are already established. After closing, you're presenting new ownership, possibly new payment terms, and new accounts payable systems. In this situation, vendor uncertainty makes the recovery of overpayments extremely difficult.

Restoring access to historical data is a complex and painful side effect of integration. Most of the time, system replacements during integration result in the permanent loss of previous data. The longer it takes to close the deal, the harder the integration side effects are.

Your system integration is disorganized. In this case, highly important areas like accounts payable recovery are bound to be neglected.

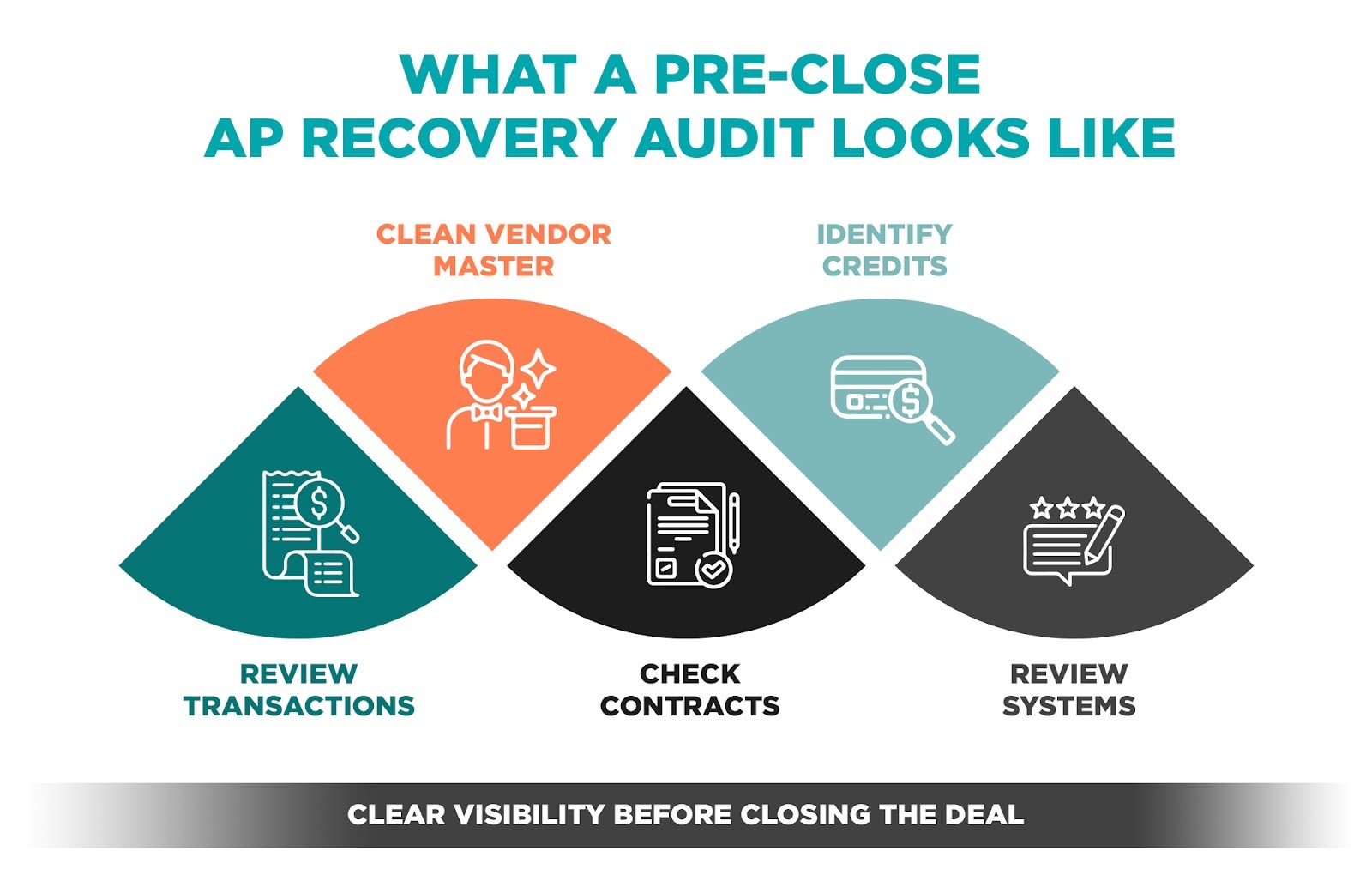

What a Pre-Close AP Recovery Audit Looks Like

Integrating accounts payable audit services into M&A due diligence can be done without compromising the deal timeline. With the right data, a focused accounts payable recovery audit can be done within 4 to 6 weeks.

The process includes:

- Transaction analysis - Review of 2 to 3 years of AP transaction history, looking for instances of duplicate payments, missing payments with a PO, and anomalous payment behaviors.

- Vendor master review - Analyze the vendor master file for duplicates, nefarious entries, and data quality issues that create a risk of leakage.

- Contract compliance assessment - Sample a vendor contract and compare it to the payment history to assess compliance and quantify the exposure.

- Open credits and debit memos - Find all vendor credit and debit memos and cash that were not applied and can be recovered.

- ERP and process review - Evaluate the effectiveness of the target's AP controls and identify gaps in the process that could lead to leakage if not addressed during the post-close period.

The output isn't just a list of problems. A comprehensive accounts payable recovery audit provides a detailed overview of recovery potential, the ongoing risk of leakage, and the process improvements necessary to avert future problems.

Final Thoughts

No M&A deal is simple, and finding post-close AP surprises that no one thought about during due diligence adds to the complexity.

Discover Dollar audit services help identify concealed liability and potential recovery in your claims as a deal approaches closing. Our AP recovery audit examines several years of transactional data, vendor records, and contracts to assess compliance and ensure potential acquirers understand the true value of their acquisition.

We help acquirers identify millions of potential recoverable value during due diligence and establish post-close AP recovery programs that enhance integration ROI. Our method, with no upfront costs and no risk, delivers results in a matter of weeks.